What are the differences between the EIS and SEIS schemes?

The Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS) were created by the British government to incentivise private investors to back early-stage companies by offering them generous tax reliefs on investment into qualifying companies or funds. These tax reliefs range from income tax relief and paying no tax on capital gains realised from the investments through to inheritance tax relief and loss relief on investments through the schemes that go bust.

While these tax efficient schemes have a lot in common, there are some important differences. These differences are most apparent when it comes to the tax reliefs offered and the developmental stage of the companies that are eligible for each scheme.

Comparison of the tax reliefs

| Income Tax Relief | Capital gains deferral | Loss relief | IHT | Tax paid on capital gains | Max annual investment |

|---|

| SEIS | 50% | Yes | Yes | Yes | 0 | £200,000 |

| EIS | 30% | Yes | Yes | Yes | 0 | £2,000,000 |

Both schemes offer investors the opportunity to defer capital gains by investing through them, both offer investors loss relief on investments that go bust, both offer investors inheritance tax relief on shares that are held for a minimum period of two years, both allow for no capital gains to be paid on profits from shares that are sold after a minimum three year period.

However, the amount of income tax relief offered by the schemes differs significantly. While both are generous, SEIS investors can receive 50% of the amount invested as income tax relief while EIS investors can receive a still healthy 30%.

In both cases, investors must hold the shares for a minimum of three years. Any shares sold, or that cease to qualify for EIS, before the holding period completes may incur tax relief clawback – where some of the initial relief must be paid back to the government.

A further difference is found in the amount investors can receive relief on each year. With the Seed Enterprise Investment Scheme, investors can claim relief on up to £200,000 invested per annum. With the Enterprise Investment Scheme, investors can claim relief on up to £1,000,000 per annum, rising to £2,000,000 per annum if at least £1m is invested in knowledge intensive companies.

Which companies qualify for SEIS and EIS?

The qualifying trades to be SEIS or EIS eligible are identical but the stage of development of the underlying companies differs slightly.

With the Seed Enterprise Investment Scheme:

A company must have under £350,000 in gross assets pre-money.

A company must have no more than 25 employees.

A company must have been trading for less than 3 years.

A company can raise up to £250k through the scheme.

A company must be carrying out a qualifying trade.

For the Enterprise Investment Scheme:

A company must have less than £15 million in gross assets pre-money.

A company must have no more than 250 employees.

A company must have been trading for less than 7 years.

A company can raise up to £12m in total (£20m if Knowledge Intensive) through the scheme.

A company can raise up to £5m (£10m if knowledge intensive) through the scheme in a given year.

A company must be carrying out a qualifying trade.

Is EIS or SEIS a better investment?

There is no right or wrong answer to this as it will ultimately come down to your risk appetite and personal tax situation. Here are a few comparison points to keep in mind:

In favour of SEIS

The income tax relief offered by the seed scheme is a fair bit higher than that offered by EIS. When it comes down to it, with the 50% in income tax relief your at risk capital on an SEIS investment is half of what you ultimately invest (up to the limit of £100k of course).

Against SEIS

The companies you invest in are generally very risky. They are incredibly early stage, most are in their first year of trading, though some may be in their second. They are small, with a maximum of 25 employees. They have very little track record and often not a lot to show for the work they’ve done. Added to the risk, they are likely to take an incredibly long time to grow and exit so if you invest through SEIS prepare for a very long haul.

In favour of EIS

While not as generous as SEIS, the income tax relief of 30% of the investment is still very significant. Companies raising through EIS can have up to 250 employees and be trading for up to seven years so they often, though not always, have some form of track record to show the investors they are pitching to. Further, as the companies can raise up to £5m in a single year they are generally better backed and have a much longer runway to build the business before needing to raise again.

Against EIS

While EIS companies are generally further along their journey than SEIS companies, the risk remains high and there is still a long way for them to go before an exit may be achieved.

How do these alternative investments impact your portfolio?

SEIS and EIS bring balance to a portfolio that has little to no exposure to venture capital. In its white paper, “The Case for Venture Capital” Invesco’s research team found that the correlation between venture capital and the large caps in the public markets is -6%. That is about as far away from 1.00 (100% correlated) and -1.00 (100% negatively correlated) as you can get without actually being 0.

When we conducted our own research that looked specifically into UK venture capital and startups we found that the correlation between the index of UK startups and the FTSE 350 is just 7%.

How can I invest in SEIS or EIS?

Both schemes allow investors to invest directly into qualifying companies or through an investment fund that then makes investments into qualifying companies.

Investing directly gives you more control over the companies you ultimately invest in and can be done online via crowdfunding, or in person through an angel network or accelerator programme. Most angels invest in ten or more companies so you’ll want to build your own portfolio if this is your preferred approach.

Investing through a fund means you don’t get to pick and choose the companies you invest in, this is left to the discretion of an experienced fund manager, but removes the burden of having to complete your own due company due diligence as well as build your own portfolio.

Details about the Access EIS Fund

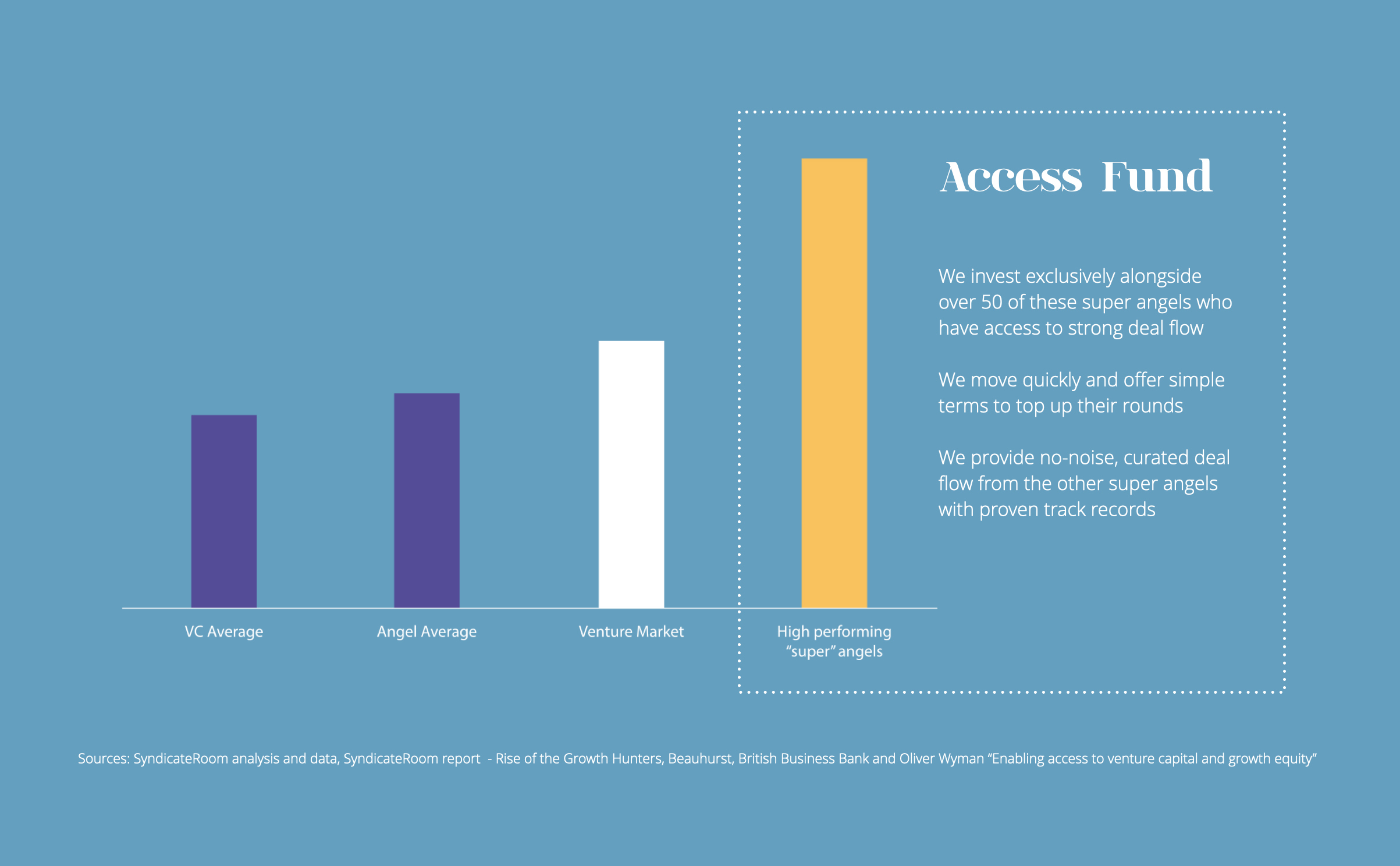

Our fund, Access EIS, tracks the performance data of over 1,000 active startup investors. It then selects and co-invests with some of the best-performing “super angels” with the aim of replicating their collective success, and diversifying your investment across at least 50 super-angel-backed startups to minimise risk and capture as many potential “blockbusters” as possible. The angels we co-invest with significantly outperform the market.

We make the process of claiming relief on multiple investments as simple as possible for our investors.

Find out more about the fund and the innovative startups we’ve backed here. If it’s right for you, we’d love to welcome you into our community of more than 500 investors.

Disclaimer

The information on this page does not constitute financial advice and is provided on an information basis only, based on research using the following sources: