How do I calculate my tax relief?

You can use our EIS calculator to get an idea of how much tax relief you would

receive on a given investment.

EIS tax relief examples.

| Company fails |

Company breaks even

|

Company doubles in value

|

|---|

| EIS investment | £10,000 | £10,000 | £10,000 |

|

Income tax relief

| -£3,000 | -£3,000 | -£3,000 |

| Net investment | £7,000 | £7,000 | £7,000 |

|

Proceeds on disposal

| £0 | £10,000 | £20,000 |

| Loss relief | -£3,150* | - | - |

| CGT payable | - | nil | nil |

|

Net profit/loss including income tax relief

| -£3,850 | £3,000 | £13,000 |

How do I claim my tax relief?

Investors claim tax relief when they complete their annual tax return, giving

details of each of their EIS qualifying investments, then submitting this to HMRC.

Alternatively, investors can complete the claim form on their EIS3 or EIS5

certificate, and submit this to HMRC. You'll need to provide HMRC with the following

information:

- The names of the companies in which you’ve invested.

- The amounts, per company, for which you’re claiming relief.

- The share issue date (often different from the date you invested).

-

The HMRC office authorising the issue of the EIS3 certificate and its reference

(as shown on the certificate).

How much can I invest into EIS?

In most cases, investors can claim tax relief on up to £1m investing in EIS eligible

companies. This increases to £2m when investing into knowledge intensive companies

(KIC)

Knowledge Intensive Companies

In the specific case of investments made into Knowledge Intensive Companies – which

are companies that put a high enough proportion of their operating costs into

research and development, create and use original intellectual property as a

significant part of the business, and/or have 20% of a higher-educated workforce

involved in R&D – investors can claim tax relief on up to £2m of investment in a

single year.

How do I invest in EIS?

Direct investments

Investing directly in startups that qualify for EIS, without going through a fund,

gives the investor more control over their choice of investments, but puts the

responsibility of due diligence and decision making over voting on company

resolutions solely in their hands. It also requires the investor to discover new

investment opportunities for themselves, so a strong network of industry contacts

can be advantageous.

Investing through a fund

Many EIS investors make their investments through funds. In this case, the fund

handles the process of selecting and investing in new opportunities. The fund builds

a portfolio for each investor in exchange for a fee.

This approach has a much lighter administrative burden for the individual investor.

Due diligence is carried out by the fund (and in the case of Access EIS, by our

super angel co-investors as well).

While the investor does not choose the individual investments, they can make a

choice about which fund to commit to. Different funds will have different approaches

to investing, some will focus on a given sector, while others will be sector

agnostic, some will build small portfolios to focus investment, others will build

larger portfolios to spread risk more widely.

It’s important to choose a fund which suits the way you want to invest, and an

approach which gives you the best chances and multiples of returns with the lowest

amount of risk. Also check the funds FCA register number to ensure they are legit.

What are the alternatives to EIS

What other types of products and services do investors consider alongside EIS, and

how are they different?

Venture Capital Trusts (VCT)

VCTs offer investors exemption from income tax on dividends on ordinary shares, and

income tax relief of 30% on the value of new ordinary shares subscribed (capped at

£200,000 per tax year) providing that shares are kept for at least five years. You

may also be able to get disposal relief through VCTs.

You can learn more about tax reliefs in our comparison of EIS vs VCTs.

The Seed Enterprise Investment Scheme (SEIS)

SEIS is a scheme similar to EIS, with the difference being that it invests in

companies at an earlier stage. Because the risk is higher, it offers income tax of

50%. But it has an annual investment limit of £100,000. You can learn more about tax

reliefs in our comparison of EIS vs SEIS.

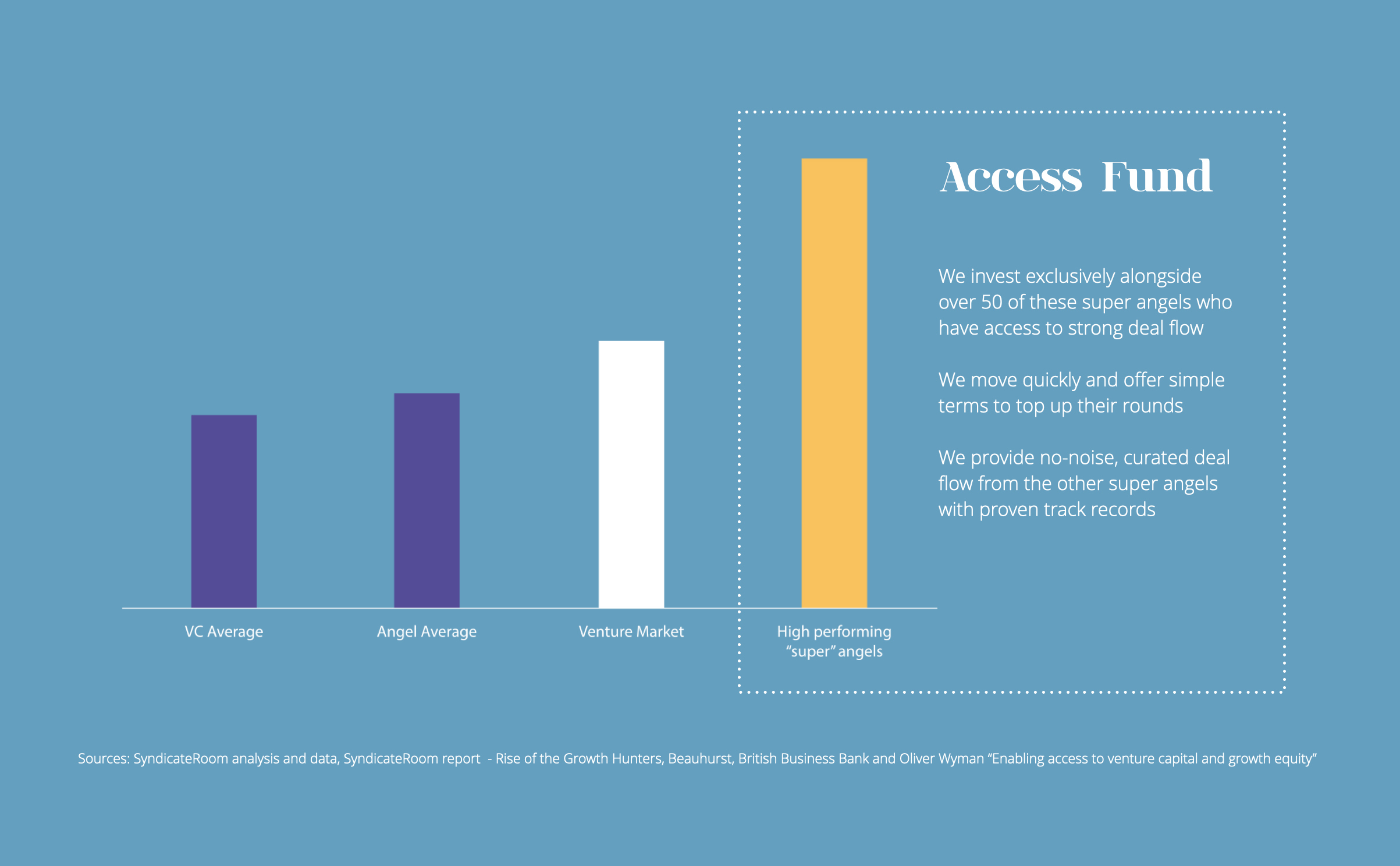

What's different about your fund, Access EIS?

Find out more about the fund and the innovative startups we've backed here. If it’s

right for you, we'd love to welcome you into our community of more than 500

investors.

The information on this page does not constitute financial advice and is provided on

an information basis only, based on research using the following sources:

- HMRC self-assessment helpsheet

- Enterprise Investment Scheme Association website

-

HMRC policy paper on the Enterprise Investment Sschme and knowledge-intensive

companies

- UK Business Angels Association guide to the Enterprise Investment Scheme