Don't invest unless you're prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

Don't invest unless you're prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. .

How to Avoid Capital Gains Tax on a Second Home (2026/27)

Selling a second home is a significant financial event and often triggers a substantial tax liability. If you are selling a property that isn't your primary residence, understanding the capital gains tax on second home sales is essential to protecting your returns.

In fact, recent legislative changes have shifted the landscape for property owners. The 2024 Autumn Budget created rate convergence, where shares and property now share the same 18%/24% capital gains tax bands. This change has removed the tax incentive to prioritise property over liquid, tax-efficient alternatives.

Below is a guide to capital gains tax on second homes. We cover current rates, allowances, and sophisticated strategies to mitigate your tax burden.

How much is the capital gains tax on a second home?

Capital Gains Tax (CGT) is paid on the profit you make when you sell an asset that has increased in value. For residential property sales in the UK, the rates are higher than for other assets like shares.

Current CGT rates (2025/26)

Following the 2024 Autumn Budget, residential property rates remain at:

Capital improvements: Costs for "enhancing" the property (e.g., an extension or new heating).

The maintenance trap: You cannot deduct general maintenance like repainting or fixing leaks. These are running costs, not capital improvements.

2. Private residence relief (PRR)

If you lived in the property as your main home at any point, you are entitled to PRR for those years.

The nine-month rule: The final nine months of ownership are tax-free if the property was ever your main residence.

The burden of proof: HMRC requires evidence of "quality of residence." Keep your address updated on the electoral roll, with your bank, and on utility bills to prove it wasn't just a temporary stay.

3. Letting relief (the "shared occupation" rule)

Since 2020, this is only available if you lived in the property at the same time as your tenant. It can provide up to £40,000 of additional relief per person.

4. Offset capital losses

If you sold other assets (like shares) at a loss this year, or have unused losses from previous years, you can "offset" them against your property gain to lower the taxable total.

5. Consider the timing of your sale

Gains are added to your income. If you expect a lower income next year (for example because of entering retirement), waiting to sell could keep more of your gain within the 18% basic-rate band rather than the 24% higher-rate band.

6. Hold-over relief (gifting)

If you gift the property (to a family member, for example), you may be able to "hold over" the gain so the recipient pays the tax only when they eventually sell it. This is complex and usually requires the property to be a business asset.

7. Advanced solution: 100% deferral via EIS or 50% reduction via SEIS

For gains that exceed your standard reliefs, the Enterprise Investment Scheme (EIS) offers a specialist escape route, giving investors the ability to defer a capital gain and treat it as having not yet arisen, for as long as they hold their EIS shares. Similarly, the Seed Enterprise Investment Scheme (SEIS) allows investors to reduce capital gains tax on gains by up to 50% if they invest an equal amount in SEIS-eligible companies.

Defer 100% of the tax: The bill is "frozen" indefinitely until you sell the EIS shares.

Gain 30% back: You receive 30% income tax credit on the amount invested.

The four-year window: You must reinvest within a window of one year before or three years after the sale.

Tax treatment depends on individual circumstances and may be subject to change.

An EIS deferral example

Value

Chargeable gain reinvested

£25,000

Tax deferred (at 24%)

£6,000

Income tax relief

£7,500

CGT reduction through SEIS reinvestment

While property sellers often confuse the two, reinvestment relief (via the Seed Enterprise Investment Scheme) is different from deferral. Investing the gain into SEIS-eligible companies allows you to:

Reduce 50% of the tax: Take what you owe on the gain and divide it by two.

Gain 50% back: You receive 50% in income tax relief on the amount invested.

No four year window With SEIS, the gain you wish to claim reinvestment relief on must arise in the same year you make your investment.

Tax treatment depends on individual circumstances and may be subject to change.

Beyond capital gains and income tax relief, investing in early-stage companies provides a "buffer" that many high-net-worth property owners use to balance their portfolios.

Loss relief: If companies fail, investors can claim relief on the remaining loss at their highest marginal rate.

IHT relief: After holding EIS shares for two years, they typically fall outside your estate for inheritance tax purposes, helping you mitigate IHT liabilities.

Which strategy fits your sale?

If your gain is...

Your best move

Under £6,000

Use joint allowances with a spouse.

£6,000 – £20,000

Maximise deductions and Private Residence Relief.

Over £20,000

Consider EIS deferral to keep 100% of your capital working or SEIS reinvestment to reduce the bill by half.

Frequently asked questions

Selling a second home creates a complex set of obligations. Below are the answers to the most frequent queries regarding the 60-day reporting window and tax-deductible costs.

1. "Can I claim Private Residence Relief (PRR) on a second home?"

You can only claim PRR for the period the property was your "only or main residence." If you have lived in the second home at any point, you may be eligible for partial relief for those years, plus the final nine months of ownership.

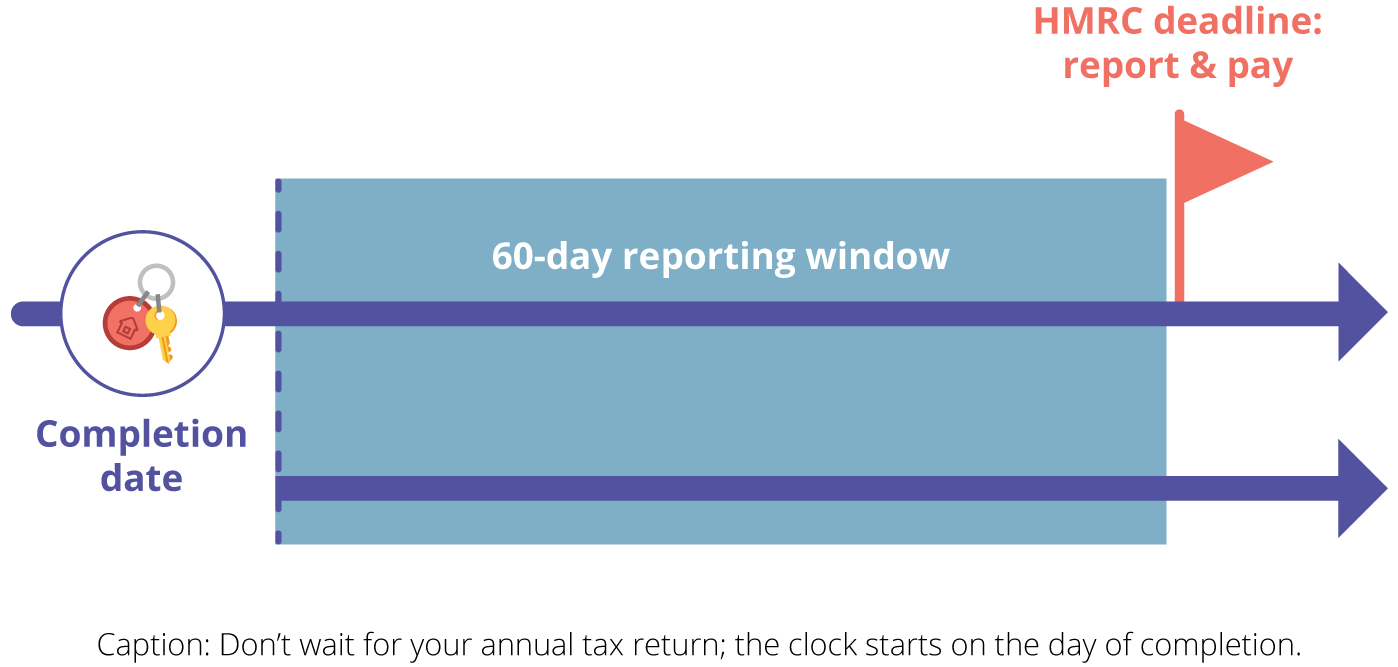

2 . "I’ve just sold my property. How long do I have to pay the tax?"

In the UK, you no longer wait until your annual Self-Assessment to pay capital gains tax on property. You must report the sale and pay the full tax amount due within 60 days of completion. Failing to meet this deadline triggers an immediate £100 penalty, followed by additional penalties and interest at the three-month and six-month marks. You can report and pay via the Gov.ukproperty reporting portal.

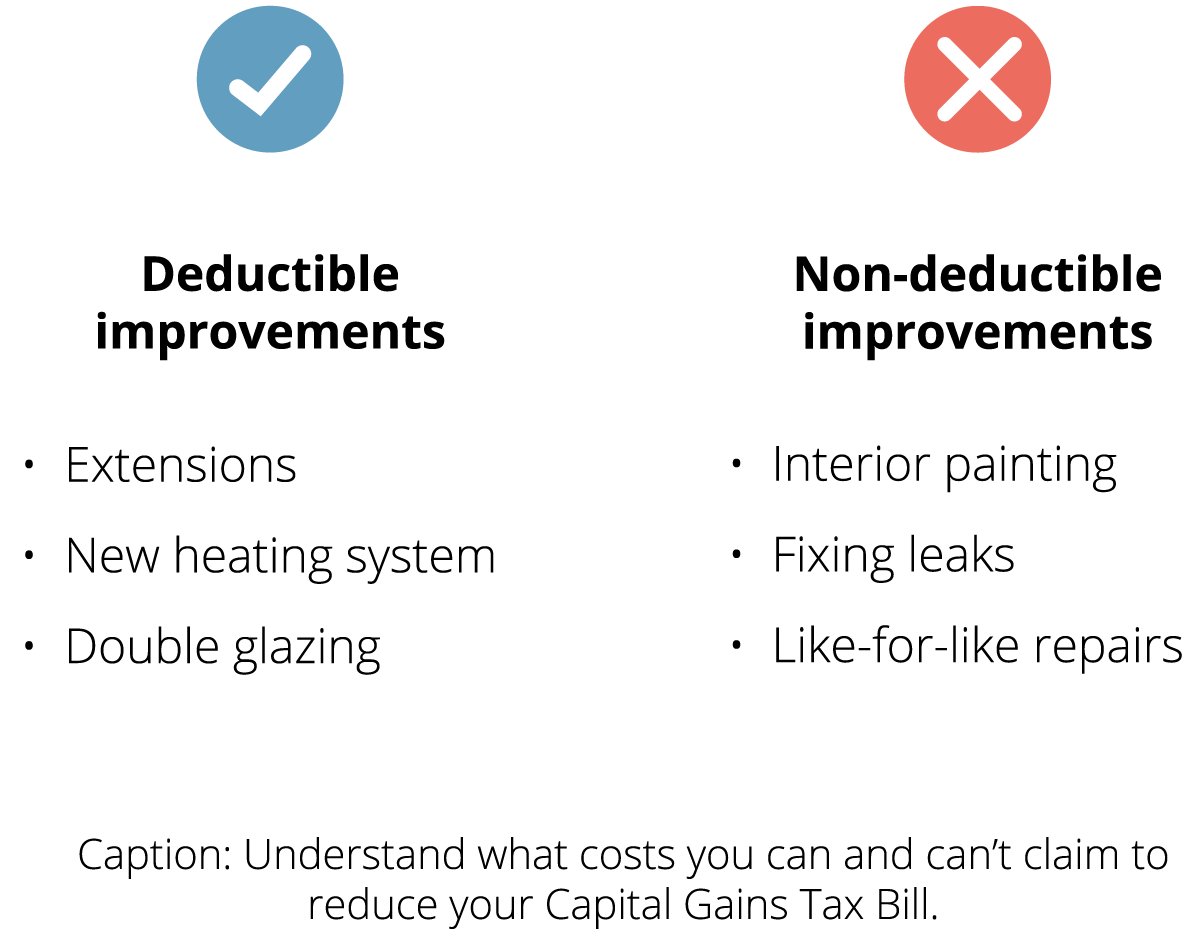

3. "What costs can I actually deduct to reduce my bill?"

To calculate your taxable gain, you don't just subtract the purchase price from the sale price. You should also deduct:

Capital improvements: You can deduct the cost of "adding value" (such as e.g., an extension, loft conversion, or installing a new central heating system).

Note on maintenance: You cannot deduct general maintenance or "wear and tear" costs, such as repainting, fixing a roof leak, or replacing a broken boiler with an identical model. These are considered running costs, not capital improvements.

4. "Can I avoid tax if I have lived in the property for a short time?"

You may be eligible for Private Residence Relief (PRR) for the period the property was your "only or main residence."

The nine-month rule: If the property was your main residence at any time, the final nine months of ownership are usually tax-free, even if you weren't living there at the time.

Nomination: If you own two homes, you have a two-year window from the date you acquire the second property to formally "nominate" which one is your primary residence for tax purposes.

5. "How does the 2024 Budget change my strategy?"

With the main CGT rates for shares now matching property (18% and 24%), the previous "tax-rate incentive" to hold property over liquid assets has vanished.

By using EIS deferral relief, you can move your capital out of a static property asset and into a diversified startup portfolio, deferring 100% of the tax bill while gaining up to 30% upfront income tax relief.

Your property disposal checklist: the next three steps

To ensure you are fully compliant and tax-optimised, we recommend the following immediate actions:

Verify your 60-day deadline: Calculate 60 days from your completion date. This is the absolute deadline to report your sale and pay the tax to HMRC via the Gov.ukproperty reporting portal.

Run a "net exposure" comparison: Before paying your bill, figure out how much you could save. Reinvesting your gain into our Access EIS Fundnot only defers the capital gain but also provides 30% upfront income tax relief. For an eligible 45% taxpayer, this can reduce your total investment exposure to just 38.5p for every £1 invested.

The Carry Back Fund gives investors the opportunity to support some of the fastest-growing Access companies on the next stage of their journey. Register to download the brochure.

Our guides & reports

See our selection of guides and reports to find out more about the benefits available to EIS and SEIS investors.

Investing in early-stage businesses involves risks, including illiquidity, lack of dividends, loss of investment and dilution, and it should be done only as part of a diversified portfolio. Tax relief depends on an individual’s circumstances and may change in the future. In addition, the availability of tax relief depends on the company invested in maintaining its qualifying status. Past performance is not a reliable indicator of future performance. You should not rely on any past performance as a guarantee of future investment performance.

This page has been approved as a financial promotion by Syndicate Room Ltd, which is authorised and regulated by the Financial Conduct Authority (No. 613021).

We use cookies to improve our service. By continuing to use this site you are agreeing to their use. Find out more. .