Are VCTs still worth it? Following changes in the 2025 Autumn Budget, from 6 April 2026, upfront income tax relief on new VCT subscriptions dropped from 30% to 20% — and the implications cut deeper than the headline suggests.

For two decades, VCTs have sold themselves on a simple pitch: accept the fees, accept the five-year lock-up, and a generous tax rebate will smooth over whatever the underlying portfolio does. Plus the potential for tax-free dividends to sweeten the deal. That pitch just got 10 percentage points weaker.

With a thinner tax cushion, investors can no longer rely on government rebates to mask high fees and mediocre returns. The change exposes a structural question that's been quietly ignored for years: once you strip away the tax wrapper, are VCTs actually delivering venture-grade returns?

This new era of venture capital demands a clinical focus on raw performance — and a hard look at whether EIS, with its unchanged 30% income tax relief and better portfolio economics, is now the smarter home for risk capital. Tax treatment depends on individual circumstances and may be subject to change.

The 2026 VCT relief cut: key facts

| Feature | VCT (Before 6 April 2026) | VCT (From 6 April 2026) | EIS (Unchanged) |

|---|

| Income tax relief | 30% | 20% | 30% |

| Max annual investment | £200,000 | £200,000 | £1,000,000 (£2m for KICs) |

| Dividend tax | 0% | 0% | 0% |

| Capital gains tax | 0% | 0% | 0% |

| Loss relief | No | No | Yes (against income tax) |

| Minimum holding period | 5 years | 5 years | 5 years |

What changed:

- Upfront income tax relief is now 20% for all new

VCT subscriptions from 6 April 2026 onward.

- The five-year rule stayed put — all VCT

investments remain locked for five years.

- Tax-free dividends and CGT exemptions on disposal

are still in place.

- VCTs purchased before the deadline retain the 30%

relief claimed at the time.

- EIS maintains 30% income tax relief with no

changes.

Why the 10% drop matters more than it looks

A 10-percentage-point reduction sounds modest

until you layer in the fee structures typical of VCTs. Annual

management fees of 2% to 3%, plus initial charges that can hit 5%,

compound over the mandatory five-year hold. These costs often exceed

the value of the government's tax relief within the holding period.

A 1% annual fee difference compounds to approximately 5% over

the five-year hold, half the relief you've just lost. Over longer

holds typical of venture capital investments, that gap widens further.

And what's more, data from the BVCA shows that nearly 85% of

venture capital firms underperform the market return of 28% IRR.

Combine fee drag with the reduced relief and sector-wide

underperformance data, and the math starts working against VCT

investors.

The case for switching to EIS

With VCT relief now at 20%, the gap between VCT and EIS has widened beyond the tax wrapper.

EIS still offers 30% upfront relief and adds loss relief against income tax if investments fail — downside protection that VCTs don't provide. But the bigger structural advantage is portfolio design.

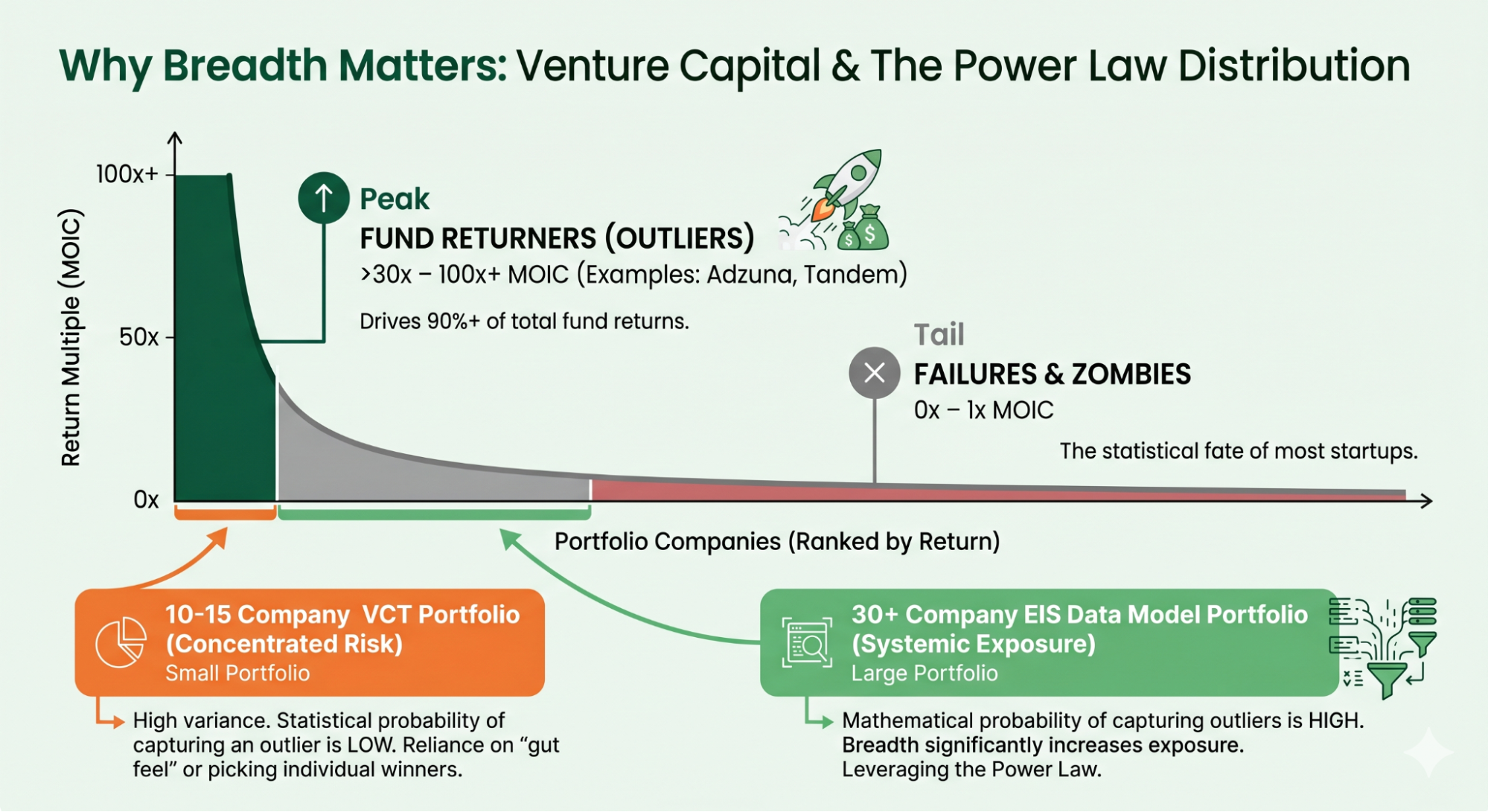

Research into the UK startup market shows that return multiples follow a power-law distribution with an exponent (alpha) of 1.8 (Graham Schwikkard, The Science of Startup Investing, 2022). A small number of companies generate the majority of returns.

The practical implication is that portfolio

size matters — but so does stage. VCTs typically hold large

portfolios of later-stage companies, where the biggest multiples

have already been compressed. Most EIS funds do the opposite: they

invest at the right stage but concentrate capital into just six to

ten companies, statistically too few to reliably catch an outlier.

Access EIS was built to close this gap. By co-investing

alongside the UK's top-performing angels, it assembles portfolios of

30+ early-stage startups — combining the stage advantage of EIS with

the diversification needed to capture power-law winners.

Investing with the UK's top-performing Angel Investors

SyndicateRoom's

Access EIS Fund

builds on a simple premise: to identify angel investors with verifiable,

top-decile track records in UK early-stage investing and co-invest alongside

them.

These aren't anonymous picks — they're angels whose portfolio

performance has been independently tracked across multiple cycles, and they've

been filtered from a dataset of thousands of UK angel investors.

For

example, one of the angels SyndicateRoom co-invests with has achieved a 126%

IRR by taking early positions in companies including Adzuna (acquired by

Recruit Holdings) and Tandem (now a publicly listed digital bank).

The

approach centres on three principles:

- Sector focus: concentrated expertise in fintech and

marketplace models rather than generalist allocation

- Early conviction: taking positions at seed or pre-seed,

before valuations inflate in later rounds

- Pro-rata rights: maintaining equity percentage through

follow-on rounds to compound on winners

This isn't luck. It's systematic access to deals most retail

investors never see, and that VCT structures may only reach in later, more

expensive rounds.

The result is a fund that targets the power-law

distribution of venture returns rather than relying on the tax wrapper to do

the heavy lifting.

When VCTs may still make sense

Despite the relief cut, VCTs retain advantages for specific

investors. Those seeking tax-free dividend income (rather than

capital growth) may still find VCTs attractive. Investors who

have maxed out their pension allowances and want liquid-ish

public-market exposure to UK small companies have fewer

alternatives. And for those uncomfortable with EIS-level

early-stage risk, the more mature company profile within a VCT

may better suit their risk appetite.

The question isn't

whether VCTs have a place — it's whether they should remain a

default choice at 20% relief.

Frequently asked questions

Will existing VCT investments be

affected?No. The reduction to 20% applies only to new

subscriptions made after 6 April 2026. Relief claimed on

existing holdings remains at the rate applicable at the time of

the investment.

What are the key differences between

VCT and EIS?VCTs invest in later-stage companies and

typically offer tax-free dividend income, with a five-year

holding period. EIS invests in earlier-stage companies and

offers higher upfront relief (30%), loss relief against income

tax if investments fail, and a shorter three-year minimum

hold. VCTs tend to suit income-focused investors; EIS tends to

suit those targeting capital growth and willing to accept

early-stage risk for higher return potential.

Can I

invest in both VCTs and EIS?

Yes. The annual

allowances are separate: £200,000 for VCTs and £1 million

for EIS (£2 million if investing in knowledge-intensive

companies). Combining both provides diversification across

company stages and tax treatment structures.

VCT vs EIS: the numbers on £100k invested

|

On £100k invested

|

VCT (new)

|

EIS

|

|---|

|

Upfront relief

|

£20,000

| £30,000 |

|

Loss relief on failures

| None |

Up to 45% of loss

|

|

Typical portfolio size

|

10–15 companies

|

30+ (diversified funds)

|

|

Minimum hold

|

5 years

|

3 years

|

Compare: EIS and VCT