Don't invest unless you're prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

Today, after two consecutive quarters of negative growth, the UK officially entered a recession. What does this mean for investors?

In the US, most venture capital firms have sent out cautionary letters to their investors and portfolio companies warning that we are entering a very lean period and that they should adjust expectations accordingly.

We ourselves are hearing from the larger UK VCs who have noticed a decline in valuation at the late-stage rounds. Part of this is because the UK has a big presence of foreign investors at the Series D stage, but also because there is a change in sentiment and indeed, lower expectations of big multiples if the company is acquired or lists on a stock exchange.

Seed-stage investors do not expect their companies to list or be acquired in the next 3–5 years and so we haven't yet seen this decline filter down to seed-stage companies. But, even if the valuation expectations don't change, a recession will impact demand and therefore impact the actual sales of seed-stage startups (if they have sales). This will lead to more of the companies failing, as well as lower valuations and paper returns for investors in the short to medium term.

Should you still invest in this market through a downturn?

We can look back at the 2020 pandemic-driven recession as an initial case, but the bounce back from that was quite quick and it didn't represent a true bear market. Indeed, we found our own cohort of 2020 investments is doing very well. In an attempt to learn from the last big bear market, we went in search of data from 2008.

Now, the venture market in the UK was vastly different 14 years ago and so was the accessibility of data. Companies House filings were mostly handwritten, and no one appears to have been making reports about the market as a whole. Having said that, we still went through as much as we could in bulk and pulled out some top line figures to share with investors. This is not perfect data, and we couldn't spend too long on cleaning it all, but I still think it tells some stories.

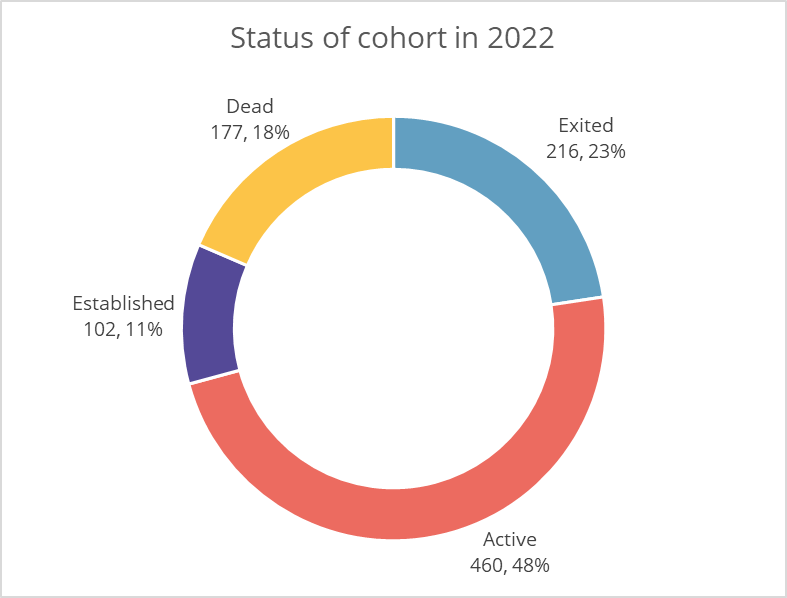

There were 953 companies that were founded between 2007 and 2009 that went on to raise at least £200k of capital. We keep it to this group that raised capital because it represents those which would have been available to investors. The current stages of these companies are listed below.

We have classified a number of these companies under growth. This simply indicates that they have raised capital in recent years and are showing activity. Established companies are showing activity for many years and are filing regular financial reports. The total valuation of all these companies is just over £18bn. Overall, there is an even spread of companies and we don't see a higher ratio of dead or exited companies than we see in other periods.

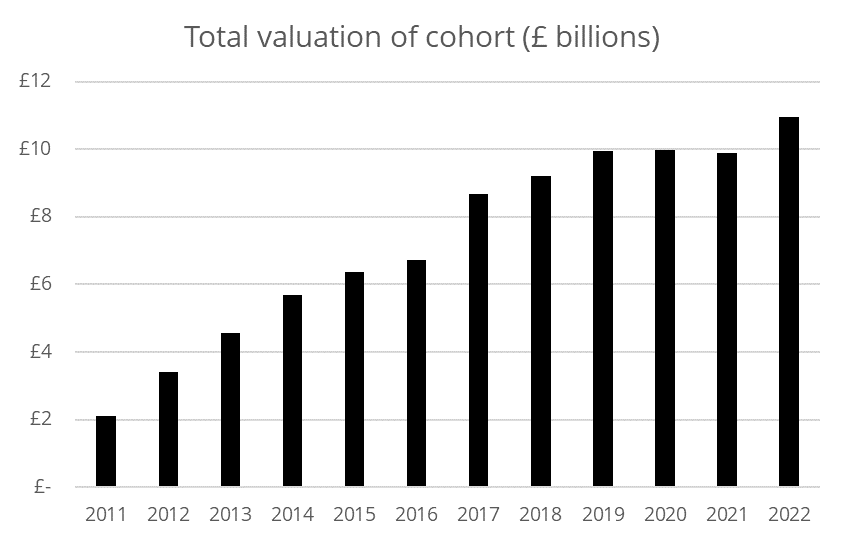

Another aspect we can look at is the growth in total valuation. I've applied an additional filter for this analysis and only included companies that raised funds within three years of being established between 2008–2009. Interestingly, the cohort did take a dip in valuations post 2020 and recovered into 2022 in line with the busy market we've seen at the start of the year. Likely driven by some of the more established companies getting large increases in valuations. Overall, the cohort grew by 5.2X, or 18% year on year in valuation.

Finally, we can always look at some of the firms that were established during this period. I've listed some of the better known ones below that would have been excellent investments at their seed stage:

So what can investors take away?

Well to start, as a fund we will continue to invest through the recession. We're not in the game of timing the market and believe there will still be 10X–100X investments at the seed stage where we are active. We bet on the market and the power law, and to succeed there you need to make a number of investments across a few cohorts. We can see that during the last great recession there were great investments to be made and even at the overall cohort level, there was good growth.

It is also worth noting that the UK venture ecosystem is a lot more developed than it was. There are a lot more startups, a lot more university spinouts, a lot more support, and a lot more investors. I've written before about the amount of dry powder that UK venture capital has, and they will be looking to deploy that capital. Therefore we would expect to see continued investment coming for all stages of growth. There may be fewer opportunities, but there will be very successful startups coming through and we don't want to miss out on those or the overall growth. Of course, we have a potentially vested interest in saying you should continue to invest, but I hope that the data that has been shared today demonstrates that it would be a good investment strategy in any case.

Find out more about our fund, Access EIS.

Please note: our office hours are weekdays, 9.30am - 5.30pm.