For most of the past two decades, a defined contribution pension was the most efficient vehicle for passing wealth to the next generation. You paid in during your working life, took what you needed in retirement, and whatever was left passed to your beneficiaries outside your taxable estate — free of inheritance tax, no seven-year clock, no conditions.

That changes on 6 April 2027.

From that date, most unused pension funds and death benefits will be included in the value of your estate for IHT purposes. For anyone who built their estate plan around leaving pension wealth to their children, the primary vehicle is gone. What remains is nine months to do something about it.

How significant is this, in practice?

For those soon to retire, or those who have just retired, with a substantial defined contribution pension — the numbers shift materially.

Take a reasonably typical picture: a 62-year-old with a pension pot of £800,000, a property worth £1.2 million, and other investments of £400,000. Total estate: £2.4 million.

Before April 2027, the pension sits outside the estate entirely. The taxable estate is £1.6 million. The combined nil rate band is £325,000, and the full residence nil rate band adds £175,000 — a £500,000 allowance in total, assuming the property passes to children. The taxable estate above the threshold is £1.1 million. At 40%, the IHT liability is £440,000.

From April 2027, the full £2.4 million is in scope. Here the taper makes things worse than the headline rate suggests: the residence nil rate band reduces by £1 for every £2 that the estate exceeds £2 million. At £2.4 million, the RNRB is cut by £200,000 — from £175,000 to nothing. The effective combined allowance drops to £325,000, the taxable estate is £2.075 million, and the IHT liability is £830,000.

The same estate. The same beneficiaries. A £390,000 difference — not a rounding error, and worse than most people's first calculation would suggest.

You can model your own position using SyndicateRoom's inheritance tax calculator, which reflects the post-April 2026 Business Relief caps as well as the pension change.

Death in service benefits paid from a registered pension scheme remain exempt after 2027, as do continuing annuities and funds under £1,000. But for the accumulated defined contribution pots that represent the primary retirement savings of most high-net-worth individuals, the exemption is removed.

This sits on top of what already changed in April 2026

The pension rule is the larger structural shift — but it lands on an estate planning environment that already changed significantly six weeks ago.

From 6 April 2026, AIM-listed shares lost their full Business Property Relief status. They now carry only 50% relief from pound one, producing an effective inheritance tax rate of 20%. For the significant number of investors who built IHT-efficient portfolios using AIM precisely because it combined liquidity with near-full relief, that logic no longer holds.

At the same time, the £2.5 million cap came into force on 100% Business Property Relief for qualifying unquoted assets, including EIS-qualifying shares. Below that threshold, unquoted EIS shares still attract 100% IHT relief after a two-year holding period. Above it, relief drops to 50%. (Unlike the pension and RNRB position above, this £2.5m cap is transferable between spouses, giving married couples up to £5m of combined 100% relief — worth bearing in mind when reading the worked example.)

Put the two changes together and the picture is stark. AIM is half the relief it was. Pension wealth is about to be fully taxable. Of the three main routes investors have used to reduce IHT exposure, two are gone or diminished. The third — Business Property Relief via unquoted qualifying assets — still works, within the cap.

The planning window is shorter than it looks

April 2027 is eleven months away. That sounds like adequate time. For pension planning it is — drawdown strategy, nomination reviews, and the interaction of pension IHT with the rest of the estate can all be modelled and adjusted before the deadline.

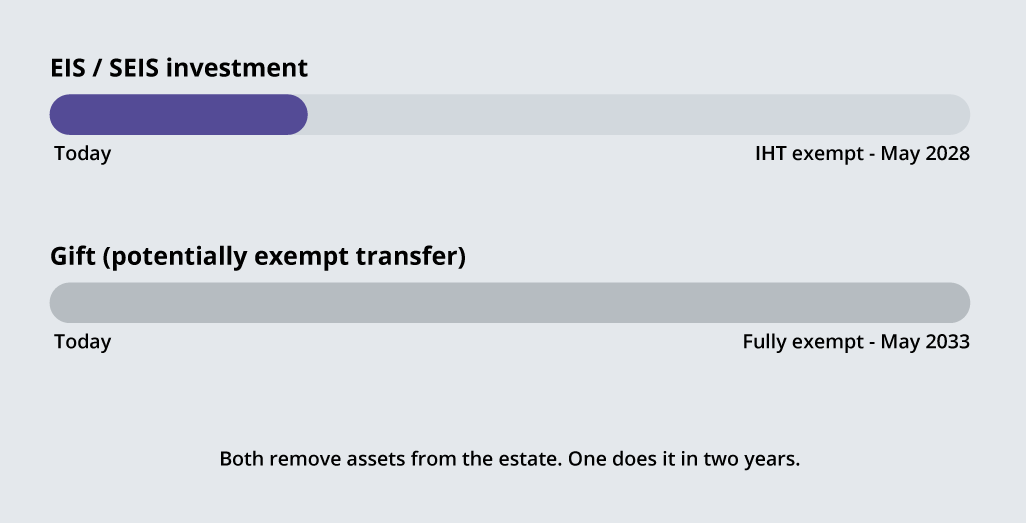

For Business Property Relief via EIS or SEIS, eleven months is tight.

Both EIS and SEIS-qualifying unquoted shares become 100% IHT exempt after a two-year holding period — but that clock runs from the date of investment. An investment made in April 2027 clears the estate in April 2029. An investment made today clears it in May 2028 — nearly a year earlier, and well inside a sensible planning horizon for someone in their late fifties or sixties.

"The investors who will be doing that modelling in a hurry next year are the same ones who could be working through it methodically today."

More practically: if the objective is to have BPR-qualifying assets in place before the pension changes bite, the two-year clock needs to start now, not when the deadline is six months away. Leaving it until early 2027 is not wrong. It simply means the relief arrives later, and for older investors the timing matters.

What a remodelled estate plan looks like

No single vehicle solves the whole problem. But a plan built for the post-April 2027 environment looks meaningfully different from one written before the Autumn Budget 2024.

On pensions, the question is drawdown strategy. The exemption is gone, but the tax-free lump sum and income drawdown mechanics still work. Spending from the pension during retirement — rather than leaving a large unused pot — reduces the IHT exposure at source. Most people haven't asked whether their current drawdown rate still makes sense under the new rules. It's the right time to ask.

Gifts remain available and unchanged. Regular gifts from surplus income are immediately outside the estate under the normal expenditure exemption. The seven-year clock for potentially exempt transfers is long, but it starts when you start it — and someone in their late fifties who begins now has a better chance of clearing the clock than someone who waits.

BPR via EIS or SEIS is the planning tool that changed least in April 2026 — and that relative stability is now its defining quality.

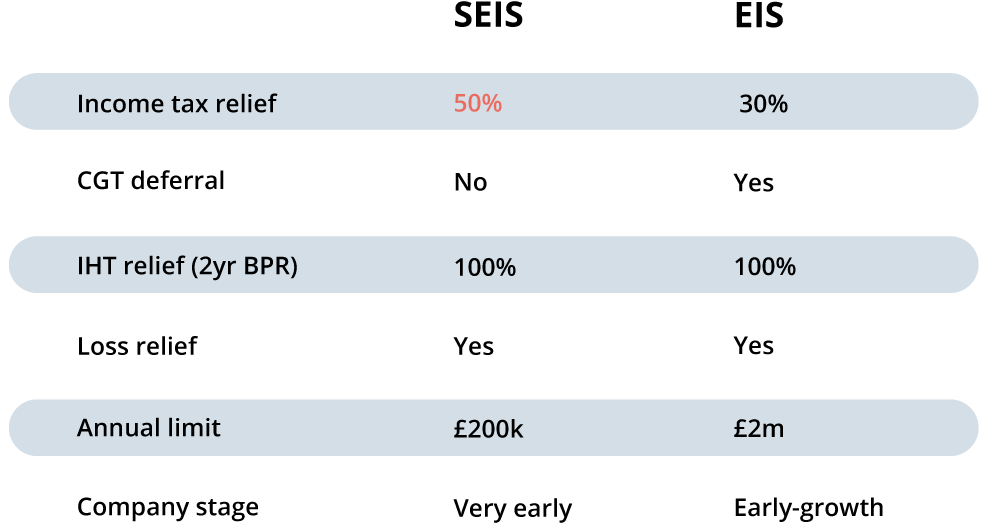

Both EIS and SEIS investments in qualifying unquoted companies become 100% IHT exempt after two years. Both offer loss relief against income rather than just capital gains. EIS adds 30% income tax relief and CGT deferral. SEIS offers 50% income tax relief on investments up to £200,000 per year — which matters particularly if the source of funds is pension drawdown, where the withdrawal will be taxed as income at 40% or 45%.

The 50% SEIS relief largely offsets that cost; EIS's 30% doesn't fully match it. But EIS is the only route that defers CGT on existing gains, which for many investors in their late fifties is equally important. The choice between them — or a mix of both — comes down to the individual's tax position. The trade-off in both cases is illiquidity and risk. That's appropriate for a defined slice of an IHT plan, not a replacement for the rest of the portfolio.

Trusts and other structures are worth discussing with your adviser alongside the above, but are beyond the scope of this article.

The interaction no plan currently models correctly

Here is the planning problem most estates will discover in 2027 if they don't address it now.

A pension pot in drawdown generates income. That income, if not spent, accumulates back into the estate — in cash, investments, or other taxable assets. Under the old rules, leaving money in the pension and drawing only what you needed was the efficient choice. Under the new rules, that logic flips: unused pension funds will carry a 40% IHT charge on death, while funds drawn down and reinvested into BPR-qualifying assets can be fully relieved after two years.

For an investor with a £600,000 pension and a meaningful IHT liability, the question has changed. It is no longer just "how much should I draw down?" It is "should some of what I draw down go straight into qualifying assets, to start the two-year BPR clock running?"

The income tax cost of drawdown is real — pension withdrawals are taxed as income, often at 40% or 45% for higher-rate taxpayers. That reduces but does not eliminate the case for redeployment. The numbers are worth showing.

Worked example: £100,000 unused pension pot on death (holder dies over 75)

Route A — leave in pension: The estate pays 40% IHT: the beneficiary inherits £60,000. When they withdraw from the remaining fund, they pay income tax at their marginal rate — at 40%, that leaves £36,000. The effective retention rate is 36p in the pound.

Route B — draw down and redeploy into EIS: Draw down £100,000 now, taxed as income at 40%: £60,000 in hand. Invest £60,000 into EIS — 30% income tax relief returns £18,000, so the net cost of the investment is £42,000. After two years, £60,000 sits entirely outside the estate. The IHT saving on that £60,000 is £24,000 (40% of £60,000). Net position: spent £42,000 to permanently remove £60,000 from the estate — and the underlying investment remains, with whatever return it generates on top.

The margin depends on individual circumstances, drawdown timing, and whether the investor dies before or after 75. But the comparison case — 36p in the pound through inaction versus a materially better position through planned redeployment — is why this question is worth modelling now rather than in 2027. The investors who will be doing that modelling in a hurry next year are the same ones who could be working through it methodically today.

SEIS or EIS — why not both?

Most discussions of S/EIS frame it as a binary choice. In the context of pension-led IHT planning, the more useful question is whether the two schemes serve different parts of the same problem.

For a higher-rate taxpayer drawing down from a pension and redeploying into qualifying assets, SEIS produces the better income tax outcome on that specific tranche. The 50% relief on a £60,000 investment returns £30,000 in income tax — effectively neutralising the 40% tax cost of the withdrawal. EIS's 30% relief on the same sum returns £18,000, leaving a net income tax drag. Both qualify for IHT relief after two years. But on the drawdown-funded portion, SEIS is more efficient.

The constraint is the annual SEIS limit: £200,000 per investor per tax year. Above that, SEIS is not available. An investor drawing down £150,000 and deploying it into qualifying assets might use the full SEIS allowance first, then direct the remainder into EIS.

£390,000

The difference in IHT liability on a £2.4m estate before and after April 2027 — on the same estate, for the same beneficiaries.

Where EIS is the better vehicle is CGT deferral. SEIS does not offer this. If the investor also holds unrealised capital gains — a common position for someone in their late fifties or sixties with a long-held investment portfolio — those gains can be deferred by rolling them into an EIS investment. The CGT liability is suspended until EIS exit, and in many cases is never crystallised at all. That benefit is unavailable through SEIS.

The practical position for many Pre-Retirees and Legacy Builders is therefore not "which scheme?" but "how much of each, and in what order?" Use SEIS to offset the income tax cost of pension drawdown. Use EIS to defer existing capital gains and accommodate larger allocations. Both start the two-year BPR clock. Both come out of the estate.

Where the Access EIS Fund and Carbon13 SEIS Fund fit

SyndicateRoom offers both schemes through dedicated funds, which can be used independently or in combination — and both are built on proprietary data rather than manager intuition.

The Access EIS Fund invests in 30 or more qualifying unquoted UK startups per deployment — diversification that reduces the single-company risk inherent in holding concentrated EIS positions. The strategy is grounded in SyndicateRoom's own research into more than 300,000 UK investor track records and 5,300 companies, which found that just 0.06% of angel investors — 183 individuals, dubbed "Super Angels" — have a proven record of 5x+ portfolio returns across portfolios of at least eight companies. The fund co-invests exclusively alongside this group, at the same time.

The 2020 and 2021 fund vintages have returned approximately 1.50x and 1.32x respectively on invested capital, based on current portfolio valuations. For an investor using EIS for CGT deferral or for allocations above the SEIS threshold, this is the relevant vehicle.

The Carbon13 SEIS Fund invests in early-stage climate technology companies qualifying under SEIS, working across sectors including energy, AI, materials, and the built environment. It is designed for investors who want 50% income tax relief on their initial investment — including those redeploying pension drawdown — alongside the standard SEIS IHT relief, loss relief, and CGT exemption on disposal. Carbon13 focuses on companies tackling the climate transition, which for some investors adds an additional dimension of purpose alongside the tax and estate planning case.

If the goal is to have BPR-qualifying assets in place before April 2027 — and to get the most out of the income tax relief along the way — a combined allocation across both funds is worth a conversation with your financial adviser.

Both funds are open for investment in the current tax year. For the two-year clock to be running before the April 2027 pension changes, an investment needs to be in place before that date. Starting this tax year means the relief arrives in 2028. Starting in 2027 means 2029.

If you'd like to understand how an EIS or SEIS allocation — or both — would interact with your estate plan and pension position, speak to your financial adviser or contact the SyndicateRoom team directly. For the underlying rules, HMRC's guidance on Business Relief and the government's policy paper on pensions and inheritance tax set out the legislative detail behind the changes discussed above.

You can explore SyndicateRoom's funds by clicking the image below: